You’re ready to take a loan. The bank approves it. Then you see the monthly number you actually have to pay — the EMI.

But what exactly is EMI? How is EMI calculated? And why does the amount change when you tweak the loan tenure or interest rate?

An Equated Monthly Instalment (EMI) is the fixed monthly payment you make to repay a loan. It includes both the principal and interest. Sounds simple. The math behind the EMI formula isn’t always.

Before you commit to any loan, you need to understand your EMI calculation, how interest is applied, and how a loan EMI calculator can help you plan smarter. Let’s break it down in plain terms.

Quick Answer: An EMI (Equated Monthly Instalment) is the fixed amount you pay every month to repay a loan, based on the loan amount, APR, and tenure. It includes both principal and interest, calculated using a standard EMI formula. Factors like interest rate, loan term, and prepayments directly affect your monthly EMI. Using a reliable loan EMI calculator helps you plan better, reduce interest costs, and borrow with confidence.

- 1 What Does EMI Mean? (Definition & Simple Explanation)

- 2 What Makes Up an EMI — Principal vs Interest

- Principal Component

- Interest Component

- Amortization Explained

- 3 How is EMI Calculated — Formula & Step-by-Step

- Why Do We Divide the Annual Rate by 12?

- Example EMI Calculation

- 4 EMI Calculator — Use & How to Use

- Why Use an EMI Calculator?

- How to Use the IxieVerse EMI Calculator

- 5 Examples of EMI for Different Loan Types

- Home Loan EMI (Mortgage)

- Personal Loan EMI

- Car Loan EMI (Auto Loan)

- Business Loan EMI (Small Business Loan)

- 6 Factors That Affect Your EMI

- Loan Amount (Principal)

- Interest Rate (APR)

- Loan Tenure (Loan Term)

- Prepayment or Part-Payment

- Floating Interest Rate Changes

- 7 How to Reduce Your EMI

- Increase Loan Tenure

- Make a Part Prepayment

- Negotiate a Lower Interest Rate

- Opt for Bullet or Step-Up EMIs

- 8 Common EMI Mistakes & How to Avoid Them

- Ignoring Processing Fees

- Missing Payments & Credit Score Impact

- Not Checking the Amortization Schedule

- Thinking “No-Cost EMI” Has No Cost

- 9 Conclusion

- 10 FAQs

- 1. How is EMI different from APR?

- 2. Does prepayment reduce EMI or loan tenure?

- 3. What happens if I miss an EMI payment?

- 4. How can I lower my monthly EMI?

- 5. Is a longer loan tenure always better?

- 6. How accurate is an online EMI calculator?

What Does EMI Mean? (Definition & Simple Explanation)

When you take a loan, the biggest question is simple: How much do I need to pay every month? That monthly payment is called an EMI.

EMI stands for Equated Monthly Instalment. It’s the fixed amount you pay to the lender every month until the loan is fully repaid. This payment includes two parts:

- Principal (the amount you borrowed)

- Interest (the cost of borrowing that money)

For borrowers, EMIs matter because they decide your monthly cash flow. If the EMI is too high, it strains your budget. If it’s manageable, you stay financially comfortable.

For lenders, EMIs ensure steady repayment. It helps them recover both the principal and interest in a structured way.

Think of EMI like rent for borrowed money.

When you rent a house, you pay a fixed amount every month. With a loan, you “rent” money from the bank — and your EMI is that fixed monthly payment.

Because the EMI amount stays predictable (in fixed-rate loans), it makes budget planning easier. You know exactly what leaves your account each month, which helps you manage savings, expenses, and other financial goals.

What Makes Up an EMI — Principal vs Interest

Most people look at their monthly EMI and assume it’s a flat repayment of the loan. It’s not that simple. Every EMI is split into two parts: principal and interest.

Understanding this split helps you see where your money is actually going — especially in the early years of a loan.

Principal Component

The principal is the actual amount you borrowed from the bank. This is the money that reduces your outstanding loan balance.

In the beginning, only a small part of your EMI goes toward the principal. As time passes, the principal component increases with each payment.

- Higher principal repayment = faster loan closure

- Lower outstanding principal = lower future interest

- Making prepayments directly reduces principal

This is why checking your amortization schedule matters.

Interest Component

The interest component is what the lender earns for giving you the loan. It’s calculated on your outstanding principal.

In most loans that follow the reducing balance EMI formula, interest is higher in the early months. That’s because your outstanding principal is still high.

Over time:

- Principal reduces

- Interest charged reduces

- More of your EMI goes toward principal

This is how the EMI calculation balances out over the loan tenure.

Amortization Explained

An amortization schedule is simply a month-by-month breakdown of your EMI.

It shows:

- Total EMI amount

- Interest paid that month

- Principal repaid that month

- Remaining loan balance

If you use a loan EMI calculator, you’ll usually see this EMI table automatically. It clearly shows how your payments shift from mostly interest to mostly principal over time.

How is EMI Calculated — Formula & Step-by-Step

Most people use a loan EMI calculator and stop there. But if you understand the EMI formula once, you’ll know exactly how your monthly payment is decided.

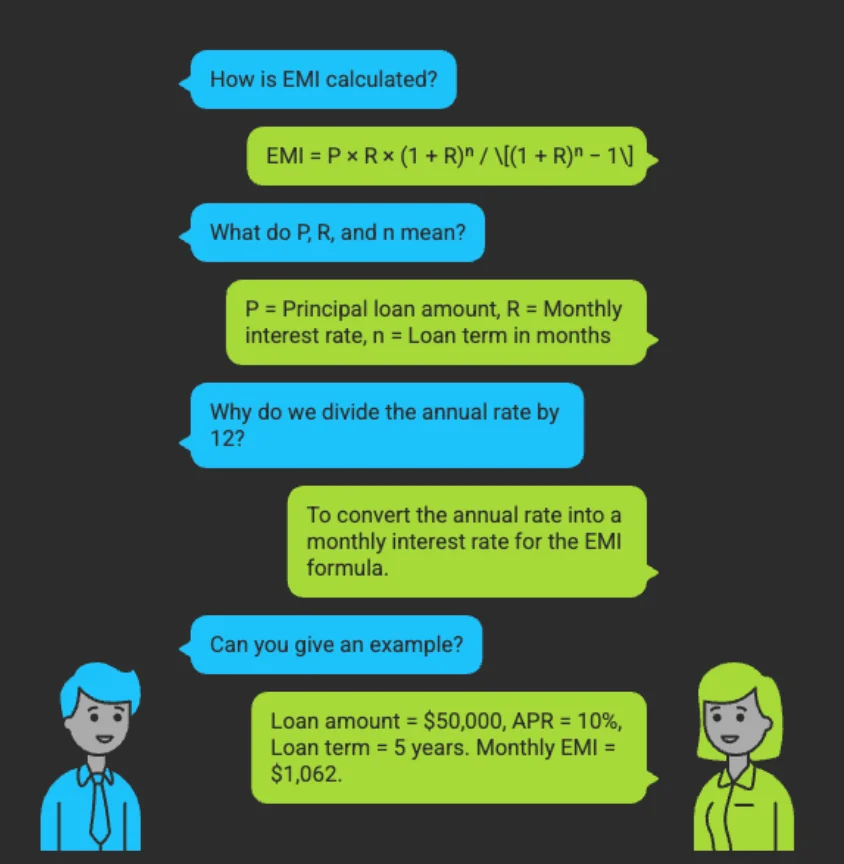

The standard EMI calculation formula is:

EMI = P × R × (1 + R)ⁿ / [(1 + R)ⁿ − 1]

Here’s what each term means:

- P = Principal loan amount (the amount you borrow)

- R = Monthly interest rate (Annual Percentage Rate ÷ 12 ÷ 100)

- n = Loan term in months

This formula is used in most loans that follow the reducing balance method — which is standard for mortgages, auto loans, and personal loans in the US.

Why Do We Divide the Annual Rate by 12?

Lenders usually advertise the APR (Annual Percentage Rate). But your EMI — or monthly loan payment — is paid every month.

So we convert the annual rate into a monthly interest rate.

Example:

- APR = 12%

- Monthly rate = 12 ÷ 12 = 1% per month

- In decimal form for the EMI formula = 0.01

That decimal value (0.01) is what goes into the formula as R.

Example EMI Calculation

Let’s break it down with real numbers.

- Loan amount (P) = $50,000

- APR = 10%

- Loan term = 5 years (60 months)

Step 1: Convert APR to monthly rate

10% ÷ 12 = 0.83% per month

In decimal = 0.0083

Step 2: Total number of months (n)

5 years × 12 = 60 months

Step 3: Apply the EMI formula

When calculated, the monthly EMI comes to approximately $1,062 per month.

That’s how lenders determine your monthly loan payment. A loan EMI calculator just automates this process, but behind the scenes, it always follows this exact EMI calculation formula.

EMI Calculator — Use & How to Use

Manually applying the EMI formula every time you compare loans is slow and confusing. One small mistake in the interest rate or tenure, and your EMI calculation goes wrong.

That’s where a loan EMI calculator saves time. It instantly shows your monthly EMI, total interest payable, and overall repayment amount.

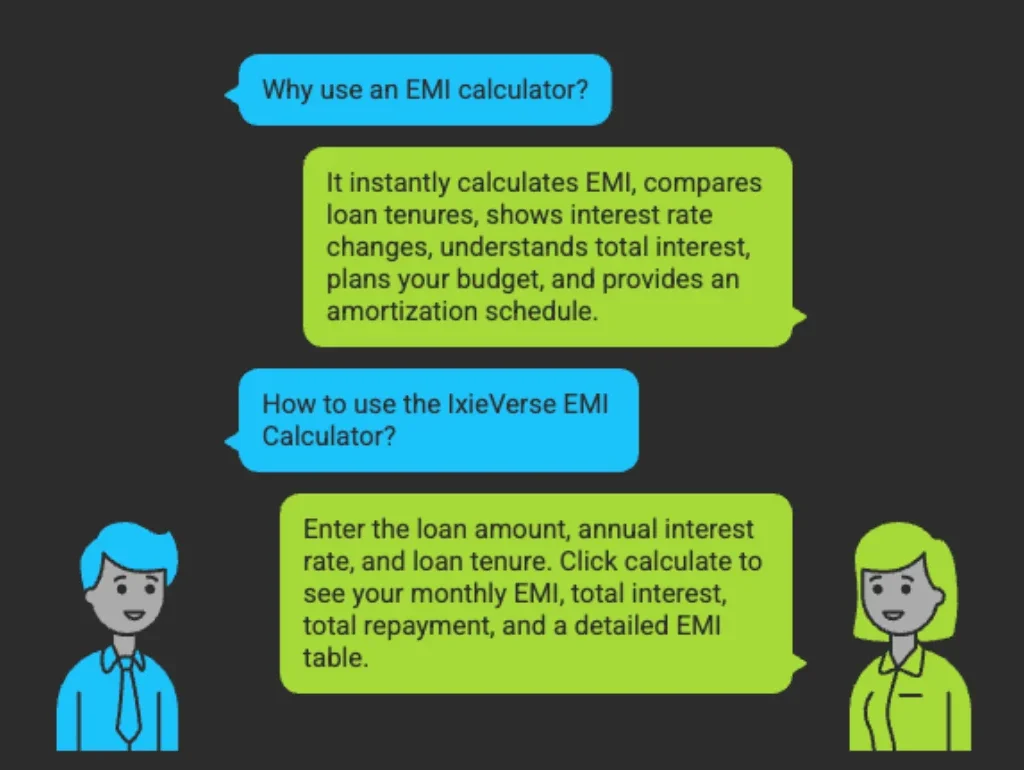

Why Use an EMI Calculator?

A good EMI calculator helps you:

- Instantly calculate EMI without doing manual math

- Compare different loan tenures

- See how interest rate changes affect your EMI

- Understand total interest paid over the loan period

- Plan your monthly budget better

It also gives you an amortization schedule, so you can clearly see the principal vs interest split.

How to Use the IxieVerse EMI Calculator

The IxieVerse EMI Calculator is designed to keep things simple. You don’t need to know the EMI formula or do any calculations.

Here’s how to use it:

- Enter the loan amount (principal)

- Add the annual interest rate

- Select the loan tenure (in months or years)

- Click calculate

Within seconds, it shows:

- Your exact monthly EMI

- Total interest payable

- Total repayment amount

- Detailed EMI table (amortization schedule)

You can adjust the interest rate or tenure and instantly see how your EMI changes. This makes it easier to choose a loan that fits your income instead of stretching your finances.

Examples of EMI for Different Loan Types

Not all EMIs are the same. Your monthly EMI depends on the loan type, interest rate (APR), and loan term.

Let’s look at how EMI calculation works across common loan types in the US.

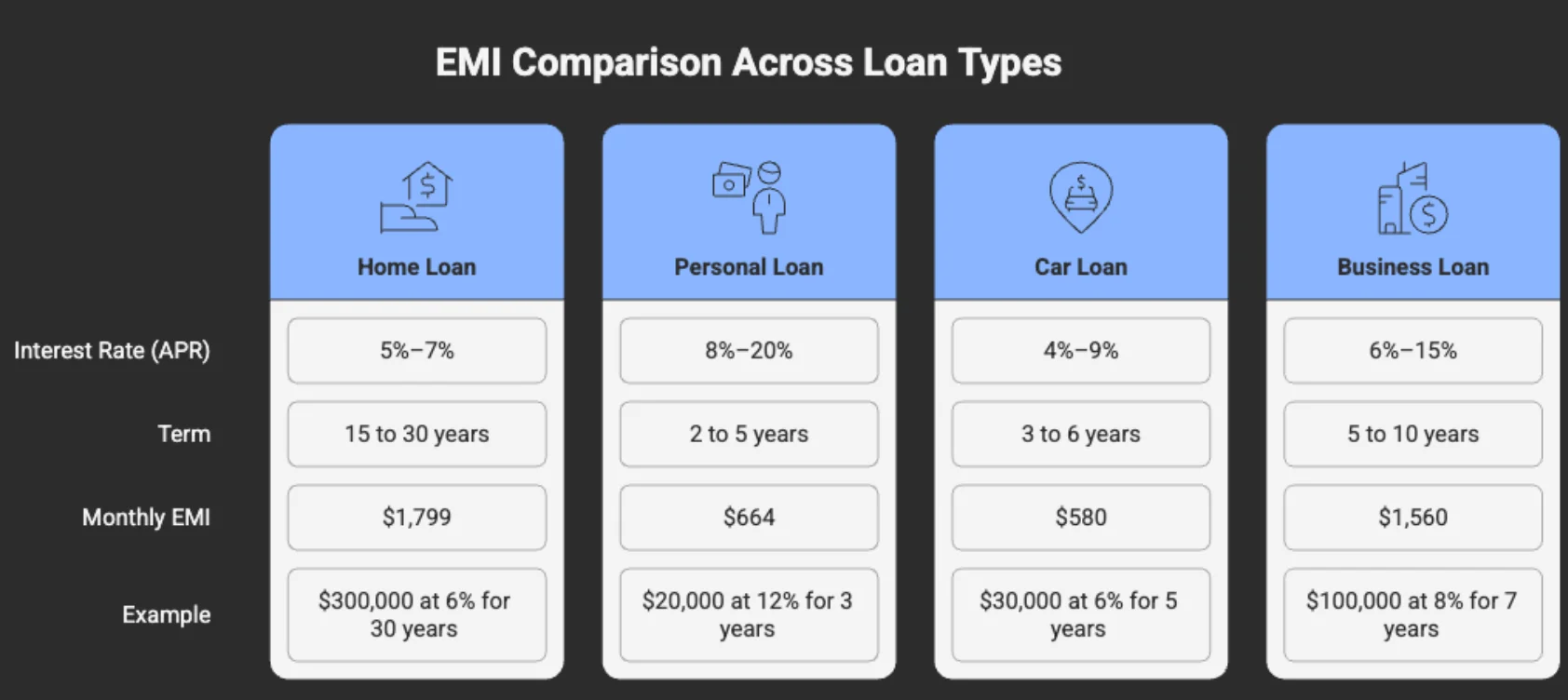

Home Loan EMI (Mortgage)

Mortgages usually have lower interest rates but long repayment terms.

Typical range in the US:

- Interest rate (APR): 5%–7%

- Term: 15 to 30 years

Because the term is long, the monthly EMI is more affordable. But you pay more interest over time.

Example:

$300,000 mortgage at 6% for 30 years

Your monthly EMI would be around $1,799 (principal + interest only).

This is why using a home loan EMI calculator before choosing a 15-year vs 30-year term is important.

Personal Loan EMI

Personal loans are unsecured, so rates are higher.

Typical range:

- APR: 8%–20%

- Term: 2 to 5 years

Because the term is shorter, the monthly EMI is higher compared to a mortgage.

Example:

$20,000 personal loan at 12% for 3 years

Your EMI would be about $664 per month.

A personal loan EMI calculator helps you adjust the loan tenure and see how it affects your monthly payment.

Car Loan EMI (Auto Loan)

Auto loans are very common in the US.

Typical range:

- APR: 4%–9% (depends on credit score)

- Term: 3 to 6 years

Your EMI depends on the loan amount and down payment. A larger down payment reduces the principal, which lowers your monthly EMI.

Example:

$30,000 auto loan at 6% for 5 years

Your EMI would be about $580 per month.

Business Loan EMI (Small Business Loan)

Small business loans or SBA loans vary based on credit, revenue, and loan program.

Typical range:

- APR: 6%–15%

- Term: 5 to 10 years (sometimes longer for SBA loans)

Example:

$100,000 business loan at 8% for 7 years

Your EMI would be roughly $1,560 per month.

For business owners, understanding the loan EMI calculation is critical. A high EMI can strain cash flow, especially in slow months.

Factors That Affect Your EMI

Your monthly EMI isn’t random. It changes based on a few key loan details. If you understand these factors, you can control your EMI calculation instead of being surprised by it.

Here’s what directly affects your EMI:

Loan Amount (Principal)

The bigger the principal loan amount, the higher your EMI.

If you borrow more, you repay more — simple as that. Even a small reduction in loan amount (like a higher down payment) can noticeably lower your monthly loan payment.

Interest Rate (APR)

Your interest rate or APR has a major impact on EMI.

- Higher APR = Higher EMI

- Lower APR = Lower EMI

- Even a 1% rate difference can change total repayment significantly

Always compare rates before finalizing a loan. Use a loan EMI calculator to see how rate changes affect your monthly cost.

Loan Tenure (Loan Term)

Tenure means how long you take to repay the loan.

- Longer term = Lower EMI, but more total interest

- Shorter term = Higher EMI, but less total interest

For example, a 30-year mortgage has a lower EMI than a 15-year mortgage — but you’ll pay much more interest overall.

Prepayment or Part-Payment

If you make extra payments toward the principal, your EMI structure changes.

Prepayment can:

- Reduce your outstanding balance

- Lower future interest

- Either reduce EMI or shorten the loan term

This directly affects your reducing balance EMI formula, since interest is calculated on the remaining principal.

Floating Interest Rate Changes

If you have a floating or variable interest rate, your EMI can increase or decrease over time.

When market rates rise:

- Your APR increases

- Your EMI increases

When rates fall:

- Your EMI may decrease

That’s why borrowers with variable-rate loans should regularly check their EMI calculation to stay prepared for changes.

How to Reduce Your EMI

Sometimes your monthly EMI feels heavier than expected. The good news? You’re not stuck with it. There are practical ways to lower your EMI — if you understand how the EMI calculation works.

Here’s what you can do:

Increase Loan Tenure

Extending your loan term spreads the repayment over more months.

- Longer tenure = Lower monthly EMI

- But total interest paid increases

- Good for short-term cash flow relief

For example, moving from a 5-year loan to a 7-year loan can significantly reduce your monthly payment — but you’ll pay more interest overall.

Make a Part Prepayment

A part prepayment reduces your outstanding principal.

Since the reducing balance EMI formula calculates interest on the remaining principal, lowering it reduces future interest.

This can:

- Lower your EMI

- Or shorten your loan tenure

- Or reduce total interest payable

Even one extra payment per year can make a noticeable difference.

Negotiate a Lower Interest Rate

Your APR (interest rate) directly impacts your EMI.

If your credit score improves or market rates drop, you can:

- Refinance your loan

- Negotiate with your lender

- Switch to a lower-rate loan

Even a 0.5%–1% reduction in interest can significantly lower your monthly loan payment.

Opt for Bullet or Step-Up EMIs

Some lenders offer flexible EMI structures.

- Step-up EMI: Lower payments initially, higher payments later

- Bullet repayment: Smaller regular EMIs with a larger lump sum at the end

These options can help if your income is expected to increase over time. Just make sure you fully understand how it affects your total repayment before choosing this route.

Common EMI Mistakes & How to Avoid Them

Most loan problems don’t happen because the EMI calculation is wrong. They happen because borrowers overlook small details. A few simple mistakes can cost you thousands over the life of a loan.

Here’s what to watch out for:

Ignoring Processing Fees

Many people focus only on the monthly EMI and forget about upfront charges.

Processing fees, origination fees, and closing costs increase the total cost of the loan, even if they’re not part of the EMI formula.

Before signing, check:

- Origination or underwriting fees

- Prepayment penalties

- Hidden administrative charges

A slightly lower EMI with high fees isn’t always the better deal.

Missing Payments & Credit Score Impact

Missing even one EMI can hurt your credit.

Late payments can:

- Lower your credit score

- Trigger late fees

- Increase your future interest rates

Your payment history directly affects future loan approvals and APR offers. Set up auto-pay if needed.

Not Checking the Amortization Schedule

Most borrowers never look at their amortization schedule.

This EMI table shows:

- How much goes toward interest

- How much reduces principal

- Your remaining loan balance

If you don’t review it, you won’t know how much interest you’re actually paying — especially in the early years.

Thinking “No-Cost EMI” Has No Cost

The phrase “no-cost EMI” sounds attractive. But in many cases, the interest is built into the product price or hidden in fees.

Always check:

- Is the product price inflated?

- Is there a processing fee?

- Is interest quietly included in the total repayment?

There’s rarely such a thing as completely free financing.

Conclusion

Most people sign a loan agreement without really understanding how their monthly EMI is calculated. That’s where mistakes happen — higher interest, longer repayment, and more stress than necessary.

When you understand the EMI formula, how the principal and interest work, and how to use a loan EMI calculator, you’re in control. It means smarter borrowing, better budgeting, and fewer surprises over time.

Before you take any loan — mortgage, auto, personal, or business — run the numbers first. Use an EMI calculator, compare APRs, check the amortization schedule, and choose a payment you can comfortably handle.

Know your EMI before you sign anything.

FAQs

1. How is EMI different from APR?

EMI is your fixed monthly loan payment.

APR (Annual Percentage Rate) is the yearly interest rate charged on your loan.

Your EMI is calculated using the APR, loan amount, and tenure.

2. Does prepayment reduce EMI or loan tenure?

Yes. A part prepayment reduces your outstanding principal.

This can:

Lower your EMI

Or shorten your loan term

And reduce total interest paid

It depends on your lender’s policy.

3. What happens if I miss an EMI payment?

Missing a monthly EMI can:

Lower your credit score

Trigger late payment fees

Increase future loan interest rates

Even one missed payment can impact your credit history.

4. How can I lower my monthly EMI?

You can reduce your EMI by:

Increasing the loan tenure

Negotiating a lower interest rate

Refinancing at a lower APR

Making part prepayments

Always compare options using a loan EMI calculator.

5. Is a longer loan tenure always better?

A longer tenure lowers your monthly EMI, but increases total interest paid.

Shorter tenure means higher EMI, but less interest overall.

It’s a trade-off between monthly comfort and total cost.

6. How accurate is an online EMI calculator?

A good EMI calculator is highly accurate if you enter the correct:

Loan amount

Interest rate (APR)

Loan tenure

It uses the standard EMI calculation formula followed by lenders.

Add a Comment